Donchian Channel StrategyIf you've read , you must be familiar with Donchian Channel Strategy. This is the second time I share this strategy because of not using English in the last publishment.

Actually, there is a build-in strategy called Channel Break Out Strategy. It is a kind of simplified version of Donchain Channel Strategy. The strategy I share today is complete Donchain Channel Strategy.

There are two differences between this strategy and Build-in Channel Break Out Strategy:

1. Channel Break Out Strategy is always in the market. According to the Channel Break Out Strategy, assuming that you held a long position at first, you will open a short position immediately if you close the long position. It is my script that makes an improvement in this aspect. You can make a distinction between closing long position and open a short position in my script and the time for entering and exiting market can be adjusted by yourself based on 4 parameters.

2. Market trends are taken into account in my script. A short Exponential Moving Average and a long Exponential Moving Average are added to this strategy. You can open a long position only when short EMA is higher then long EMA. On the contrary, short EMA being lower then long EMA is a prerequisite for open a short position.

You can adjust 4 parameters in my script. In the end, I'd like to remind you that different combination of parameters applies to different time period. The default parameters may fit 30M candle and you can try combination of 8-4-5-15 in 1D candle. Of course, you can try another combination of parameters in other time period.

I will write some simple strategies in the future if time allows. So, welcome to follow me if my script can profit you. Happy trading!

"the strat" için komut dosyalarını ara

Understanding order sizestype: properties manipulation, no programming needed

time required: 15minutes, at least

level: medium (need to know contracts, trading pairs)

A strategy can "appear" to work or be broken depending on the pile of cash that is working on. This amount is defined in the strat properties, under "order size".

For noobs (like me) this is very confusing at first :)

A strat opens/closes positions using units, a generic measure for the chart being operated on. Thes "units" can be a fixed amount of cash, a fixed amount of contracts, or a floating amount based on the last profits made. I recommend checking my previous strat to figure the case of contracts .

So, any trading price is the amount of "things" you get for some "cash". The things are the first unit, the "cash" is the second. Some examples:

XAU/USD - 1 xau oz is worth x dollars

BTC/USD - 1 bitcoin is worth x dollars

GBP/EUR - 1 pound is worth x euros

To add to confusion, a lot of markets the "unit size" is different from what the strat thinks it is. An options contract is 100 shares(the unit), 1 xau contract is 10 oz(units), 1 eur/usd contract is 100k euros and so on... so, after figuring out how the sizes work in a strat, then the sizes must be adapted for the specific market in question.

The choice os using the ETHUSD pair is because:

1 - you can buy 1eth, unlike a gold contract for example, so 1 "unit" = 1 eth, easier to get

2 - ETH is around 12 bucks, wich gives round numbers on the math, easier to wrap the brains around :)

3- is an unusual pair, so the regular contract sizes don't apply, and the brain is not conditioned to work inside the box ;)

You will have to access the script properties, to change the values. As these values are changed you will see exactly the differences in the values of the strat.

Text is too long, check the comments for all the cases

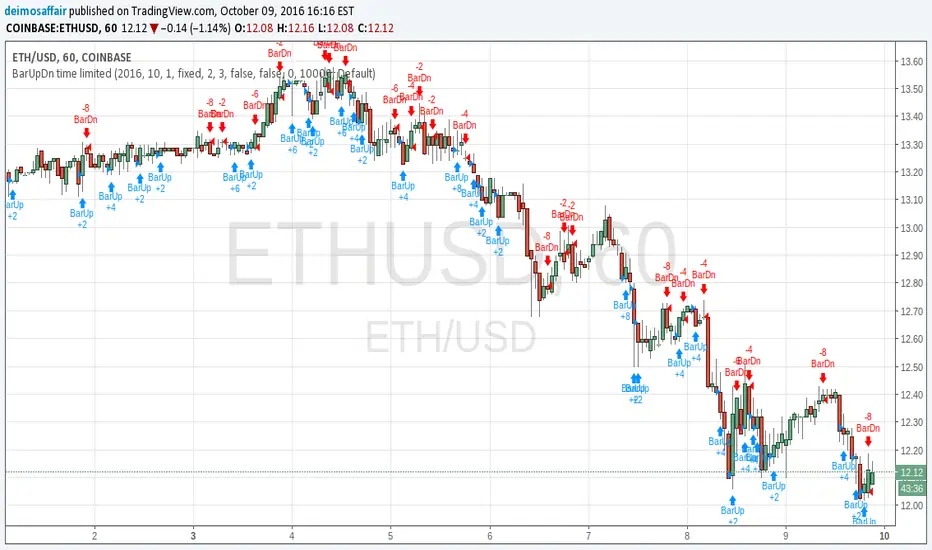

Understanding contract sizes in a strategyThis simple strat fires up on green bars, down on red bars. cannot get any simpler. So, it's a good example to check how returns are calculated.

First, the internal firing mechanism for the strategy.entry function is something hardcore. As result, the entry points can be confusing, and seem to appear in a wrong bar (as the 2nd and 3rd signals are good examples), but i'll put that aside to keep it simple. And, because i don't yet get it myself ;)

The example is simple, so that numbers can be followed easy. Chart in BTC/USD, so USD is the "base" currency used by strat to calculate. A contract/unit is the value of 1 unit in base currency. 1 Apple share is 600$, 1 bitcoin is 600$, 1 oz gold is 1330 bucks. So, here in each bar, the value of 1 contract is the value of the BTC in USD. simple as that.

The strat properties, can be passed as input fields (line 2) or accessed/changed in the right click->properties pop-up. To make it easier, initial capital is 1000 bucks, and "order size" is 1 contract. This means that the strat will open a position of 1 BTC when it fires. Value "Initial capital" makes no difference at all, at least with these choices. It's just for show. Try to put 1$ and 1 contract, the strat will still trade anyway. It manages to trade 1 contract(or BTC) values at ~600$, with a single dollar. nice ;)

Check the chart. see the little blue "BarUp +1" ? that's it, strat goes long 1 BTC. there's a little blue triangle on the bar, points to the value of entry.

Then later, on second move, the "BarDn -2", the strat goes short 2BTC. 1BTC to close the long +1 more to open a short.

The profit here is the difference between the value of the long opening and the long closing. The extra BTC (shorted) is part of the next position. Since this dumb strat just reverses the direction, there are always +2, -2 , +2.... 1 to close previous position, 1 to open another. At the strategy tester tab, the option "list of trades" shows in details each of the moves

Checking each move and comparing what we see with the chart itself helps to achieve ilumination :)

Bonus feature: as soon as you get it, try to increase the option "pyramiding" and see how the strat adds more contracts, and how it reverses the positions. sometimes it even makes sense!!!! :)

Super-AO with Risk Management Strategy Template - 11-29-25Super-AO Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to the Super-AO Strategy. This is more than just a buy/sell indicator; it is a complete, open-source Risk Management (RM) Template designed for the Pine Script community.

At its core, this script implements a robust swing-trading strategy combining the SuperTrend (for macro direction) and the Awesome Oscillator (for momentum). However, the real power lies under the hood: a custom-built Risk Management Engine that handles trade states, prevents repainting, and manages complex exit conditions like Staged Take Profits and Advanced Adaptive Trailing Stops (AATS).

We are releasing this code to help traders transition from simple indicators to professional-grade strategy structures.

2. Quick Action Guide (TL;DR)

Best Timeframe: 4 Hours (H4) and above. Designed for Swing Trading.

Best Assets: "Well-behaved" assets with clear liquidity (Major Forex pairs, BTC, ETH, Indices).

Strategy Type: Trend Following + Momentum Confirmation.

Key Feature: The Risk Management Engine is modular. You can strip out the "Super-AO" logic and insert your own strategy logic into the template easily.

Repainting: Strictly Non-Repainting. The engine calculates logic based on confirmed candle closes.

3. Detailed Report: How It Works

A. The Strategy Logic: Super-AO

The entry logic is based on the convergence of two classic indicators:

SuperTrend: Determines the overall trend bias (Green/Red).

Awesome Oscillator (AO): Measures market momentum.

The Signal:

LONG (+2): SuperTrend is Green AND AO is above the Zero Line AND AO is Rising.

SHORT (-2): SuperTrend is Red AND AO is below the Zero Line AND AO is Falling.

By requiring momentum to agree with the trend, this system filters out many false signals found in ranging markets.

B. The Risk Management (RM) Engine

This script features a proprietary State Machine designed by Signal Lynx. Unlike standard strategies that simply fire orders, this engine separates the Signal from the Execution.

Logic Injection: The engine listens for a specific integer signal: +2 (Buy) or -2 (Sell). This makes the code a Template. You can delete the Super-AO section, write your own logic, and simply pass a +2 or -2 to the RM_EngineInput variable. The engine handles the rest.

Trade States: The engine tracks the state of the trade (Entry, In-Trade, Exiting) to prevent signal spamming.

Aggressive vs. Conservative:

Conservative Mode: Waits for a full trend reversal before taking a new trade.

Aggressive Mode: Allows for re-entries if the trend is strong and valid conditions present themselves again (Pyramiding Type 1).

C. Advanced Exit Protocols

The strategy does not rely on a single exit point. It employs a "Layered Defense" approach:

Hard Stop Loss: A fixed percentage safety net.

Staged Take Profits (Scaling Out): The script allows you to set 3 distinct Take Profit levels. For example, you can close 10% of your position at TP1, 10% at TP2, and let the remaining 80% ride the trend.

Trailing Stop: A standard percentage-based trailer.

Advanced Adaptive Trailing Stop (AATS): This is a highly sophisticated volatility stop. It calculates market structure using Hirashima Sugita (HSRS) levels and Bollinger Bands to determine the "floor" and "ceiling" of price action.

If volatility is high: The stop loosens to prevent wicking out.

If volatility is low: The stop tightens to protect profit.

D. Repainting Protection

Many Pine Script strategies look great in backtesting but fail in live trading because they rely on "real-time" price data that disappears when the candle closes.

This Risk Management engine explicitly pulls data from the previous candle close (close , high , low ) for its calculations. This ensures that the backtest results you see match the reality of live execution.

4. For Developers & Modders

We encourage you to tear this code apart!

Look for the section titled // Super-AO Strategy Logic.

Replace that block with your own RSI, MACD, or Price Action logic.

Ensure your logic outputs a 2 for Buy and -2 for Sell.

Connect it to RM_EngineInput.

You now have a fully functioning Risk Management system for your custom strategy.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

This code has been in action since 2022 and is a known performer in PineScript v5. We provide this open source to help the community build better, safer automated systems.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

Multi-Endeks KAMA & RSI Stratejisi v6 (Long & Short)Multi-Index KAMA & RSI Strategy v6 (Long & Short)

This is a hybrid trading strategy that combines two powerful technical analysis tools—the Kaufman's Adaptive Moving Average (KAMA) for trend following and the Relative Strength Index (RSI) for measuring momentum and identifying overbought/oversold conditions.

The term "Multi-Index" suggests that the decision-making process might incorporate data or conditions from several different market indices or timeframes, rather than just the single asset being traded.

🧭 Core Components

1. KAMA (Kaufman's Adaptive Moving Average)

KAMA is an adaptive moving average developed by quantitative financial theorist Perry J. Kaufman.

Adaptivity: Unlike standard moving averages, KAMA automatically adjusts its smoothing factor (speed) based on market volatility.

Mechanism:

Trending Markets (Low Noise): When prices move clearly in one direction (low volatility), KAMA speeds up, hugging the price closely and providing fast signals.

Sideways Markets (High Noise): When prices are choppy (high volatility/noise), KAMA slows down, smoothing out price fluctuations to reduce the risk of whipsaws (false signals).

Role in Strategy: To define the main trend direction. The position of the price relative to the KAMA line determines the base directional bias (Long or Short).

2. RSI (Relative Strength Index)

RSI is a momentum oscillator developed by J. Welles Wilder Jr. that measures the speed and change of price movements.

Overbought/Oversold: It oscillates between 0 and 100. Conventionally, a reading above 70 suggests overbought conditions (potential sell signal), and a reading below 30 suggests oversold conditions (potential buy signal).

Role in Strategy: Timing and Confirmation. Once the trend is confirmed by KAMA, the RSI acts as a timing filter, often confirming an entry as it moves away from extreme overbought (for Short) or oversold (for Long) levels.

📉 Potential Trading Logic (V6)

This "v6" strategy likely aims to capture more reliable entries by requiring both trend (KAMA) and momentum (RSI) alignment:

1. LONG (Buy) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be above the KAMA line (confirming an uptrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross above the 30 level (exiting oversold) or decisively move above the 50 level.

Option B (Trend-Continuation): In a strong uptrend, the RSI might bounce off the 40-50 zone and turn upwards, confirming trend continuation.

2. SHORT (Sell) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be below the KAMA line (confirming a downtrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross below the 70 level (exiting overbought) or decisively move below the 50 level.

Option B (Trend-Continuation): In a strong downtrend, the RSI might be rejected from the 50-60 zone and turn downwards, confirming continuation.

3. Exit Management

The strategy likely utilizes dynamic risk controls:

Stop-Loss: A dynamic stop placed on the opposite side of the KAMA, or an ATR-based distance to adjust to volatility.

Take-Profit: Conditions such as the RSI reaching extreme levels or the KAMA line being crossed in the reverse direction.

🌟 Implication of the "V6" Version

The "v6" designation implies that the strategy has been refined and iterated upon over time to address weaknesses in prior versions (v1, v2, etc.). These improvements might include:

Filters: Adding stricter RSI or KAMA cross filters to reduce false signals.

Multi-Index Logic: Using the RSI or KAMA of a secondary instrument (e.g., a major index or volatility measure) as a macro filter for the main trade execution.

Optimization: Optimizing the default lookback periods for KAMA and RSI for different asset classes.

PA Builder [PrimeAutomation]1. PA Builder – Overview

PA Builder is not a fixed strategy; it’s a framework for building strategies. Instead of giving traders one rigid system, it provides a toolbox where entries, exits, filters, risk parameters, and automation rules can all be defined and combined. The core philosophy is confluence: the idea that a trade should only be taken when multiple independent signals agree. The Builder is built around this principle. Every module; trend, reactors, bands, reversals, volume, structure, divergences, externals can be treated as one layer of confidence. The stronger the alignment across layers, the higher the quality of the setup in theory.

In practice, this means PA Builder encourages traders to think in terms of “confluence,” not single indicators. Trend and positioning define whether you should even be looking for longs or shorts. Timing tools such as bands, reversals and candlestick structures determine when inside that broader bias you want to engage. Confirmation tools like volume and flow tell you whether capital is actually supporting the move. Filter systems then ensure that even if everything looks good locally, you still respect higher-timeframe or opposing warnings. The Builder’s philosophy is simple: enter less often, but only when conditions are genuinely in your favour.

2. Core Entry Signal Components

The entry logic in PA Builder is built on a set of signal engines that can be combined in many ways. Trend Signals form a natural foundation. They use low-lag low-pass filters, borrowed from audio signal processing, to extract directional bias from price without the classic delay of classical moving averages. The sensitivity parameter controls how reactive this engine is: lower values favour cleaner trends and fewer whipsaws, while higher values are better suited to short-term intraday trading where speed matters more than smoothness. Many traders start by requiring that Trend Signals show “all bullish” or “all bearish” before allowing any entries in that direction.

Trend signals firing short positions

On top of this directional backbone, the Dynamic Reactor behaves as an adaptive baseline. It accelerates in volatile phases and slows down during consolidation, effectively acting as a moving reference point for both trend and price position. A typical use of this module is to insist that, for long trades, the price sits above a bullish reactor; for shorts, below a bearish one. At the higher-timeframe level, the Quantum Reactor provides a VWAP-style reference that can be anchored to larger candles than the chart you are trading. A common configuration is to trade on a 15-minute chart while requiring that price is above the 4-hour Quantum Reactor for longs or below it for shorts. The “fast” and “slow” options determine how quickly this reference adapts to new information.

Timing is then refined with tools like Quantum Bands, reversals and candle structure analysis. Quantum Bands identify extremes within the current environment. In an uptrend, a tag of the lower band can be treated as a pullback rather than a breakdown; in a downtrend, the upper band acts like a shorting zone. Many traders combine “trend up and above higher-timeframe reactor” with “price temporarily below lower band” to construct a mean-reversion entry inside a larger uptrend. Reversal detection modules examine recent bars to find turning points, with shorter lookbacks capturing fast flips and longer lookbacks tracking deeper structural changes. Candle structure logic goes beyond classical candlestick names and instead focuses on whether price action confirms follow-through or reversion behaviour, with options like “2X” modes that wait for two successive confirmations before acting.

Before and after filtering using reactor applied.

Additional confirmation layers come from Volume Matrix, Money Flow, OSC True7 and divergence detection. Volume and flow tools answer whether actual capital is participating in the move or whether price is drifting on thin activity. OSC True7 categorises the state of the trend into intuitive buckets, strong, healthy, neutral, or exhausted, making it easier to avoid chasing extremes. Divergences between price and momentum can be used either as entry triggers in contrarian systems or as hard filters that block trades when warning signs are present. Finally, two external indicator inputs make it possible to integrate RSI, MACD, custom indicators or even other strategies into the Builder, either as simple thresholds or as comparative logic between two external sources (for example, requiring a fast EMA to be above a slow EMA before allowing longs).

3. Exit System & Trade Management

The exit systems in PA Builder are designed to be as vital as the entry logic. It assumes exits are not an afterthought, but half of the edge. Instead of forcing a single take profit point, the system uses a three-tier structure where you can assign different portions of the position to different targets. A common pattern is to scale out a small portion early (for example at one ATR), another portion at an intermediate level, and keep the largest slice for a deeper move. This creates a natural balance: you book something early to reduce emotional stress, while leaving room to participate in the full potential of a trend.

Targets can be defined using ATR multiples or risk-to-reward ratios that are directly tied to the initial stop distance. Using ATR keeps exits proportional to current volatility. A two ATR target in a quiet environment is very different in absolute price distance from the same multiple in a high-volatility environment, yet conceptually it represents the same “size” move. Risk-to-reward exits build on this by ensuring that if you risk one unit (1R), the reward targets are set at predefined multiples of that risk. This enforces positive expectancy at the structural level: the strategy cannot generate entries with inherently negative payoffs.

Once price begins to move in your favour, trailing logic takes over if you choose to enable it. Trailing can begin immediately from entry or only after a target has been hit. Many users prefer to let TP1 and TP2 behave as fixed profit points and then apply a trailing stop or trailing take profit to the final remainder. That way, routine winners are banked mechanically, while occasional explosive moves can be ridden for as long as the market allows. The breakeven module supports this behaviour by automatically moving stops to entry (or slightly through entry into profit) after a specified condition such as TP1 being hit. This transforms the risk profile mid trade: once breakeven has been secured, remaining size can be managed with much less psychological pressure.

The system also recognises the cost of time. Kill Switch functionality exits trades that have been open too long under mediocre conditions, typically when they are in modest profit but not progressing. This protects you from capital being tied up while better opportunities appear elsewhere. Underlying all of this are several trailing stop mechanisms: percentage-based, tick-based for very short-term strategies, TP linked trailing that activates only once a certain profit threshold has been achieved, and ATR based trailing that automatically scales the trail distance with volatility. Each method serves a slightly different profile of strategy, but all share the same aim: preserve gains and limit downside in a structured way rather than rely on discretionary judgement after the fact.

4. Filters and Risk Management

The filter systems in PA Builder formalise the idea that good trading is often about knowing when not to act. “Do Not Trade” conditions can be configured so that even a perfectly aligned bullish entry stack is overridden if certain bearish evidence is present. These can include higher timeframe reversal structures, powerful opposing divergences, or conflicting signals in key modules. By assigning conditions specifically to “Do Not Long” and “Do Not Short” rather than only to entries, you create asymmetry: buying requires bullish evidence and an absence of strong bearish warnings; selling requires the mirror.

Volatility filters extend this logic to the regime level. Some strategies are inherently suited to low volatility, range bound environments where fading extremes is profitable; others require expansion and energy to function properly. By binding trading permission to volatility ranges, you ensure that a mean-reversion system does not blindly attempt to fade a breakout, and that a momentum system does not spin its wheels in a dead, sideways market. You can even reference volatility from a higher timeframe than the one you trade, so that a five-minute strategy is still aware of the broader one-hour volatility regime it sits inside.

Applied DO NOT TRADE - removes poor signal

Risk management and position sizing are configured so each trade is expressed in units of risk rather than arbitrary size. Leverage, in this framework, is simply a scaling factor for capital efficiency; the actual risk per trade is still controlled by the distance between entry and stop and the percentage of equity you choose to expose. Reinvestment options then decide what proportion of accumulated profit is fed back into position sizing. A more aggressive reinvestment setting accelerates compounding but increases the amplitude of drawdowns; a more conservative one smooths the equity curve at the cost of slower growth. The Base Trade Value parameter ties all of this together by deciding how much nominal capital or how many contracts are committed per trade in light of your maximum allowed simultaneous positions and your intended use of leverage.

External exit conditions provide further flexibility. For example, you might design a system whose entries rely purely on PA Builder’s internal modules, but whose exits use RSI readings, moving average crosses, or a proprietary external indicator. The separation of entry and exit logic allows you to bolt on different behaviours at the tail end of trades while keeping your core signal engine intact. In all cases, the objective is the same: express risk in a controlled, repeatable way that can survive long stretches of unfavourable market conditions.

5. PDT, Cooldowns and Visual Modes

For traders subject to Pattern Day Trading rules, PA Builder includes a day-trade tracking system that counts business days correctly and respects the three-trades-in-five-days limit. This goes beyond simple compliance; it forces discipline. When intraday trading is heavily constrained, you are naturally pushed toward swing-oriented strategies with fewer, more selective entries. The tool visually marks your PDT status so you never inadvertently cross the line and trigger a lockout.

Cooldown systems address another reality: psychological vulnerability after streaks. Following several consecutive wins, many traders unconsciously loosen their standards, take marginal signals, oversize positions, or overtrade. A win-streak cooldown deliberately pauses trading after a configured number of wins, giving you time to reset. The same applies to losing streaks. After a run of losses, the strongest temptation is often to “make it back now,” which is exactly when discipline is weakest. A loss-streak cooldown enforces a break in activity during this high-risk emotional state, helping to prevent cascading damage driven by revenge trading.

Visualisation comes in two main modes. Classic mode emphasises precision: it draws explicit entry lines, stop levels, target levels and fill zones, making it easy to audit risk/reward on each trade, verify that the exit logic behaves as intended, and review historical trades in detail. Modern mode emphasises market feel: instead of focusing on exact levels, it colours candles and backgrounds to reflect momentum, profit state and dynamics.

This helps you see at a glance whether a strategy is operating in a smooth trending environment or a choppy, fragmented one, and whether current trades are broadly working or struggling. Many users develop and debug in Classic mode and then monitor live performance in Modern mode, so both representations become part of the workflow.

6. Strategy Design Workflow, Examples and Cautions

Designing with PA Builder is inherently iterative. You begin with a simple theory and a minimal configuration, perhaps just a trend filter and a basic stop/target structure, and run a backtest. You then examine where the system fails. If you see many losses occurring in counter-trend conditions, you add an additional directional filter or restrict entries with a higher-timeframe reactor condition. If you observe many small whipsaw losses, you might require candle structure confirmation or volume confirmation before allowing an entry. Each change is made one at a time and evaluated. This process gradually builds a layered system where every component has a clear purpose: some reduce drawdown, some increase win rate, some cut out only the worst trades, and others help capture more of the best ones.

A conservative swing strategy might need an agreement between short-term trend signals, a higher-timeframe Quantum position, and a bullish Dynamic Reactor state, while checking that volume supports the move and that no significant bearish reversals or divergences are present on higher timeframes. It might accept relatively few trades, but each trade would be tightly controlled, scaled out over several ATR-based targets and protected with breakeven and trailing logic. On the opposite end, an aggressive scalping configuration would relax some filters, favour faster sensitivities, use short lookback reversals, and tighten stops and targets dramatically, relying on high frequency and careful volatility filtering to maintain edge.

Throughout all of this, overfitting remains the main danger. The more parameters you tune and the more coincidental rules you add to make the backtest equity curve smoother, the more likely it is that you are capturing noise rather than a real, repeatable edge. Signs of overfitting include heavily optimised numeric values with no intuitive justification, large differences between in-sample and out-of-sample results, or strategies that work spectacularly in very specific regimes and collapse elsewhere. To mitigate this, keep strategies as simple as possible, test across different market regimes (bull, bear, range), and accept that robust systems usually look less “perfect” on the historical chart.

Bridging the gap from backtest to live trading is another critical step. Before risking capital, it is wise to paper trade the configuration for a number of trades to confirm that signal frequency, behaviour and execution align with expectations. When going live, starting with minimal size and gradually scaling up based on real-world performance helps manage both financial and psychological risk. If live results diverge significantly from backtest expectations due to slippage, fees, or changing market conditions, you can adjust, reduce size, or temporarily pause rather than commit fully to a failing configuration.

Ultimately, PA Builder is designed to be a tool for building structured, rules-driven trading systems. It gives you the tools to express your ideas, test them, refine them, and run them under controlled risk. It does not remove uncertainty or guarantee results, but it does provide a clear, transparent way to translate trading concepts into executable, testable logic, and to evolve those systems as markets change and your understanding deepens.

ATH대비 지정하락률에 도착 시 매수 - 장기홀딩 선물 전략(ATH Drawdown Re-Buy Long Only)본 스크립트는 과거 하락 데이터를 이용하여, 정해진 하락 %가 발생하는 경우 자기 자본의 정해진 %만큼을 진입하게 설계되어진 스트레티지입니다.

레버리지를 사용할 수 있으며 기본적으로 셋팅해둔 값이 내장되어있습니다.(자유롭게 바꿔서 쓰시면 됩니다.) 추가적으로 2번의 진입 외에도 다른 진입 기준, 진입 %를 설정하실 수 있으며 - ChatGPT에게 요청하면 수정해줄 것입니다.

실제 사용용도로는 KillSwitch 기능을 꺼주세요. 바 돋보기 기능을 켜주세요.

ATH Drawdown Re-Buy Long Only 전략 설명

1. 전략 개요

ATH Drawdown Re-Buy Long Only 전략은 자산의 역대 최고가(ATH, All-Time High)를 기준으로 한 하락폭(드로우다운)을 활용하여,

특정 구간마다 단계적으로 롱 포지션을 구축하는 자동 재매수(Long Only) 전략입니다.

본 전략은 다음과 같은 목적을 가지고 설계되었습니다.

급격한 조정 구간에서 체계적인 분할 매수 및 레버리지 활용

ATH를 기준으로 한 명확한 진입 규칙 제공

실시간으로

평단가

레버리지

청산가 추정

계좌 MDD

수익률

등을 시각적으로 제공하여 리스크와 포지션 상태를 직관적으로 확인할 수 있도록 지원

※ 본 전략은 교육·연구·백테스트 용도로 제공되며,

어떠한 형태의 투자 권유 또는 수익을 보장하지 않습니다.

2. 전략의 핵심 개념

2-1. ATH(역대 최고가) 기준 드로우다운

전략은 차트 상에서 항상 가장 높은 고가(High)를 ATH로 기록합니다.

새로운 고점이 형성될 때마다 ATH를 갱신하고, 해당 ATH를 기준으로 다음을 계산합니다.

현재 바의 저가(Low)가 ATH에서 몇 % 하락했는지

현재 바의 종가(Close)가 ATH에서 몇 % 하락했는지

그리고 사전에 설정한 두 개의 드로우다운 구간에서 매수를 수행합니다.

1차 진입 구간: ATH 대비 X% 하락 시

2차 진입 구간: ATH 대비 Y% 하락 시

각 구간은 ATH가 새로 갱신될 때마다 한 번씩만 작동하며,

새로운 ATH가 생성되면 다시 “1차 / 2차 진입 가능 상태”로 초기화됩니다.

2-2. 첫 포지션 100% / 300% 특수 규칙

이 전략의 중요한 특징은 **“첫 포지션 진입 시의 예외 규칙”**입니다.

전략이 현재 어떠한 포지션도 들고 있지 않은 상태에서

최초로 롱 포지션을 진입하는 시점(첫 포지션)에 대해:

기본적으로는 **자산의 100%**를 기준으로 포지션을 구축하지만,

만약 그 순간의 가격이 ATH 대비 설정값 이상(예: 약 –72.5% 이상 하락한 상황) 이라면

→ 자산의 300% 규모로 첫 포지션을 진입하도록 설계되어 있습니다.

이 규칙은 다음과 같이 동작합니다.

첫 진입이 1차 드로우다운 구간에서 발생하든,

첫 진입이 2차 드로우다운 구간에서 발생하든,

현재 하락폭이 설정된 기준 이상(예: –72.5% 이상) 이라면

→ “이 정도 하락이면 첫 진입부터 더 공격적으로 들어간다”는 의미로 300% 규모로 진입

그 이하의 하락폭이라면

→ 첫 진입은 100% 규모로 제한

즉, 전략은 다음 두 가지 모드로 동작합니다.

일반적인 상황의 첫 진입: 자산의 100%

심각한 드로우다운 구간에서의 첫 진입: 자산의 300%

이 특수 규칙은 깊은 하락에서는 공격적으로, 평소에는 상대적으로 보수적으로 진입하도록 설계된 것입니다.

3. 전략 동작 구조

3-1. 매수 조건

차트 상 High 기준으로 ATH를 추적합니다.

각 바마다 해당 ATH에서의 하락률을 계산합니다.

사용자가 설정한 두 개의 드로우다운 구간(예시):

1차 구간: 예를 들어 ATH – 50%

2차 구간: 예를 들어 ATH – 72.5%

각 구간에 대해 다음과 같은 조건을 확인합니다.

“이번 ATH 구간에서 아직 해당 구간 매수를 한 적이 없는 상태”이고,

현재 바의 저가(Low)가 해당 구간 가격 이하를 찍는 순간

→ 해당 바에서 매수 조건 충족으로 간주

실제 주문은:

해당 구간 가격에 맞춰 롱 포지션 진입(리밋/시장가 기반 시뮬레이션) 으로 처리됩니다.

3-2. ATH 갱신과 진입 기회 리셋

차트 상에서 새로운 고점(High)이 기존 ATH를 넘어서는 순간,

ATH가 갱신되고,

1차 / 2차 진입 여부를 나타내는 내부 플래그가 초기화됩니다.

이를 통해, 시장이 새로운 고점을 돌파해 나갈 때마다,

해당 구간에서 다시 한 번씩 1차·2차 드로우다운 진입 기회를 갖게 됩니다.

4. 포지션 사이징 및 레버리지

4-1. 계좌 자산(Equity) 기준 포지션 크기 결정

전략은 현재 계좌 자산을 다음과 같이 정의하여 사용합니다.

현재 자산 = 초기 자본 + 실현 손익 + 미실현 손익

각 진입 구간에서의 포지션 가치는 다음과 같이 결정됩니다.

1차 진입 구간:

“자산의 몇 %를 사용할지”를 설정값으로 입력

설정된 퍼센트를 계좌 자산에 곱한 뒤,

다시 전략 내 레버리지 배수(Leverage) 를 곱하여 실제 포지션 가치를 계산

2차 진입 구간:

동일한 방식으로, 독립된 퍼센트 설정값을 사용

즉, 포지션 가치는 다음과 같이 계산됩니다.

포지션 가치 = 현재 자산 × (해당 구간 설정 % / 100) × 레버리지 배수

그리고 이를 해당 구간의 진입 가격으로 나누어 실제 수량(토큰 단위) 를 산출합니다.

4-2. 첫 포지션의 예외 처리 (100% / 300%)

첫 포지션에 대해서는 위의 일반적인 퍼센트 설정 대신,

다음과 같은 고정 비율이 사용됩니다.

기본: 자산의 100% 규모로 첫 포지션 진입

단, 진입 시점의 ATH 대비 하락률이 설정값 이상(예: –72.5% 이상) 일 경우

→ 자산의 300% 규모로 첫 포지션 진입

이때 역시 다음 공식을 사용합니다.

포지션 가치 = 현재 자산 × (100% 또는 300%) × 레버리지

그리고 이를 가격으로 나누어 실제 진입 수량을 계산합니다.

이 규칙은:

첫 진입이 1차 구간이든 2차 구간이든 동일하게 적용되며,

“충분히 깊은 하락 구간에서는 첫 진입부터 더 크게,

평소에는 비교적 보수적으로” 라는 운용 철학을 반영합니다.

4-3. 실레버리지(Real Leverage)의 추적

전략은 각 바 단위로 다음을 추적합니다.

바가 시작할 때의 기존 포지션 크기

해당 바에서 새로 진입한 수량

이를 바탕으로, 진입이 발생한 시점에 다음을 계산합니다.

실제 레버리지 = (포지션 가치 / 현재 자산)

그리고 차트 상에 예를 들어:

Lev 2.53x 와 같은 형식의 레이블로 표시합니다.

이를 통해, 매수 시점마다 실제 계좌 레버리지가 어느 정도였는지를 직관적으로 확인할 수 있습니다.

5. 시각화 및 모니터링 요소

5-1. 차트 상 시각 요소

전략은 차트 위에 다음과 같은 정보를 직접 표시합니다.

ATH 라인

High 기준으로 계산된 역대 최고가를 주황색 선으로 표시

평단가(평균 진입가) 라인

현재 보유 포지션이 있을 때,

해당 포지션의 평균 진입가를 노란색 선으로 표시

추정 청산가(고정형 청산가) 라인

포지션 수량이 변화하는 시점을 감지하여,

당시의 평단가와 실제 레버리지를 이용해 근사적인 청산가를 계산

이를 빨간색 선으로 차트에 고정 표시

포지션이 없거나 레버리지가 1배 이하인 경우에는 청산가 라인을 제거

매수 마커 및 레이블

1차/2차 매수 조건이 충족될 때마다 해당 지점에 매수 마커를 표시

"Buy XX% @ 가격", "Lev XXx" 형태의 라벨로

진입 비율과 당시 레버리지를 함께 시각화

레이블의 위치는 설정에서 선택 가능:

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

5-2. 우측 상단 정보 테이블

차트 우측 상단에는 현재 계좌·포지션 상태를 요약한 정보 테이블이 표시됩니다.

대표적으로 다음 항목들이 포함됩니다.

Pos Qty (Token)

현재 보유 중인 포지션 수량(토큰 기준, 절대값 기준)

Pos Value (USDT)

현재 포지션의 시장 가치 (수량 × 현재 가격)

Leverage (Now)

현재 실레버리지 (포지션 가치 / 현재 자산)

DD from ATH (%)

현재 가격 기준, 최근 ATH에서의 하락률(%)

Avg Entry

현재 포지션의 평균 진입 가격

PnL (%)

현재 포지션 기준 미실현 손익률(%)

Max DD (Equity %)

전략 전체 기간 동안 기록된 계좌 기준 최대 손실(MDD, Max Drawdown)

Last Entry Price

가장 최근에 포지션을 추가로 진입한 직후의 평균 진입 가격

Last Entry Lev

위 “Last Entry Price” 시점에서의 실레버리지

Liq Price (Fixed)

위에서 설명한 고정형 추정 청산가

Return from Start (%)

전략 시작 시점(초기 자본) 대비 현재 계좌 자산의 총 수익률(%)

이 테이블을 통해 사용자는:

현재 계좌와 포지션의 상태

리스크 수준

누적 성과

를 직관적으로 파악할 수 있습니다.

6. 시간 필터 및 라벨 옵션

6-1. 전략 동작 기간 설정

전략은 옵션으로 특정 기간에만 전략을 동작시키는 시간 필터를 제공합니다.

“Use Date Range” 옵션을 활성화하면:

시작 시각과 종료 시각을 지정하여

해당 구간에 한해서만 매매가 발생하도록 제한

옵션을 비활성화하면:

전략은 전체 차트 구간에서 자유롭게 동작

6-2. 진입 라벨 위치 설정

사용자는 매수/레버리지 라벨의 위치를 선택할 수 있습니다.

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

이를 통해 개인 취향 및 차트 가독성에 맞추어

시각화 방식을 유연하게 조정할 수 있습니다.

7. 활용 대상 및 사용 예시

본 전략은 다음과 같은 목적에 적합합니다.

현물 또는 선물 롱 포지션 기준 장기·스윙 관점 추매 전략 백테스트

“고점 대비 하락률”을 기준으로 한 규칙 기반 운용 아이디어 검증

레버리지 사용 시

계좌 레버리지·청산가·MDD를 동시에 모니터링하고자 하는 경우

특정 자산에 대해

“새로운 고점이 형성될 때마다

일정한 규칙으로 깊은 조정 구간에서만 분할 진입하고자 할 때”

실거래에 그대로 적용하기보다는,

전략 아이디어 검증 및 리스크 프로파일 분석,

자신의 성향에 맞는 파라미터 탐색 용도로 사용하는 것을 권장합니다.

8. 한계 및 유의사항

백테스트 결과는 미래 성과를 보장하지 않습니다.

과거 데이터에 기반한 시뮬레이션일 뿐이며,

실제 시장에서는

유동성

슬리피지

수수료 체계

강제청산 규칙

등 다양한 변수가 존재합니다.

청산가는 단순화된 공식에 따른 추정치입니다.

거래소별 실제 청산 규칙, 유지 증거금, 수수료, 펀딩비 등은

본 전략의 계산과 다를 수 있으며,

청산가 추정 라인은 참고용 지표일 뿐입니다.

레버리지 및 진입 비율 설정에 따라 손실 폭이 매우 커질 수 있습니다.

특히 **“첫 포지션 300% 진입”**과 같이 매우 공격적인 설정은

시장 급락 시 계좌 손실과 청산 리스크를 크게 증가시킬 수 있으므로

신중한 검토가 필요합니다.

실거래 연동 시에는 별도의 리스크 관리가 필수입니다.

개별 손절 기준

포지션 상한선

전체 포트폴리오 내 비중 관리 등

본 전략 외부에서 추가적인 안전장치가 필요합니다.

9. 결론

ATH Drawdown Re-Buy Long Only 전략은 단순한 “저가 매수”를 넘어서,

ATH 기준으로 드로우다운을 구조적으로 활용하고,

첫 포지션에 대한 **특수 규칙(100% / 300%)**을 적용하며,

레버리지·청산가·MDD·수익률을 통합적으로 시각화함으로써,

하락 구간에서의 규칙 기반 롱 포지션 구축과

리스크 모니터링을 동시에 지원하는 전략입니다.

사용자는 본 전략을 통해:

자신의 시장 관점과 리스크 허용 범위에 맞는

드로우다운 구간

진입 비율

레버리지 설정

다양한 시나리오에 대한 백테스트와 분석

을 수행할 수 있습니다.

다시 한 번 강조하지만,

본 전략은 연구·학습·백테스트를 위한 도구이며,

실제 투자 판단과 책임은 전적으로 사용자 본인에게 있습니다.

/ENG Version.

This script is designed to use historical drawdown data and automatically enter positions when a predefined percentage drop from the all-time high occurs, using a predefined percentage of your account equity.

You can use leverage, and default parameter values are provided out of the box (you can freely change them to suit your style).

In addition to the two main entry levels, you can add more entry conditions and custom entry percentages – just ask ChatGPT to modify the script.

For actual/live usage, please turn OFF the KillSwitch function and turn ON the Bar Magnifier feature.

ATH Drawdown Re-Buy Long Only Strategy

1. Strategy Overview

The ATH Drawdown Re-Buy Long Only strategy is an automatic re-buy (Long Only) system that builds long positions step-by-step at specific drawdown levels, based on the asset’s all-time high (ATH) and its subsequent drawdown.

This strategy is designed with the following goals:

Systematic scaled buying and leverage usage during sharp correction periods

Clear, rule-based entry logic using drawdowns from ATH

Real-time visualization of:

Average entry price

Leverage

Estimated liquidation price

Account MDD (Max Drawdown)

Return / performance

This allows traders to intuitively monitor both risk and position status.

※ This strategy is provided for educational, research, and backtesting purposes only.

It does not constitute investment advice and does not guarantee any profits.

2. Core Concepts

2-1. Drawdown from ATH (All-Time High)

On the chart, the strategy always tracks the highest high as the ATH.

Whenever a new high is made, ATH is updated, and based on that ATH the following are calculated:

How many percent the current bar’s Low is below the ATH

How many percent the current bar’s Close is below the ATH

Using these, the strategy executes buys at two predefined drawdown zones:

1st entry zone: When price drops X% from ATH

2nd entry zone: When price drops Y% from ATH

Each zone is allowed to trigger only once per ATH cycle.

When a new ATH is created, the “1st / 2nd entry possible” flags are reset, and new opportunities open up for that ATH leg.

2-2. Special Rule for the First Position (100% / 300%)

A key feature of this strategy is the special rule for the very first position.

When the strategy currently holds no position and is about to open the first long position:

Under normal conditions, it builds the position using 100% of account equity.

However, if at that moment the price has dropped by at least a predefined threshold from ATH (e.g. around –72.5% or more),

→ the strategy will open the first position using 300% of account equity.

This rule works as follows:

Whether the first entry happens at the 1st drawdown zone or at the 2nd drawdown zone,

If the current drawdown from ATH is at or below the threshold (e.g. –72.5% or worse),

→ the strategy interprets this as “a sufficiently deep crash” and opens the initial position with 300% of equity.

If the drawdown is less severe than the threshold,

→ the first entry is capped at 100% of equity.

So the strategy has two modes for the first entry:

Normal market conditions: 100% of equity

Deep drawdown conditions: 300% of equity

This special rule is intended to be aggressive in extremely deep crashes while staying more conservative in normal corrections.

3. Strategy Logic & Execution

3-1. Entry Conditions

The strategy tracks the ATH using the High price.

For each bar, it calculates the drawdown from ATH.

The user defines two drawdown zones, for example:

1st zone: ATH – 50%

2nd zone: ATH – 72.5%

For each zone, the strategy checks:

If no buy has been executed yet for that zone in the current ATH leg, and

If the current bar’s Low touches or falls below that zone’s price level,

→ That bar is considered to have triggered a buy condition.

Order simulation:

The strategy simulates entering a long position at that zone’s price level

(using a limit/market-like approximation for backtesting).

3-2. ATH Reset & Entry Opportunity Reset

When a new High goes above the previous ATH:

The ATH is updated to this new high.

Internal flags that track whether the 1st and 2nd entries have been used are reset.

This means:

Each time the market makes a new ATH,

The strategy once again has a fresh opportunity to execute 1st and 2nd drawdown entries for that new ATH leg.

4. Position Sizing & Leverage

4-1. Position Size Based on Account Equity

The strategy defines current equity as:

Current Equity = Initial Capital + Realized PnL + Unrealized PnL

For each entry zone, the position value is calculated as follows:

The user inputs:

“What % of equity to use at this zone”

The strategy:

Multiplies current equity by that percentage

Then multiplies by the strategy’s leverage factor

Thus:

Position Value = Current Equity × (Zone % / 100) × Leverage

Finally, this position value is divided by the entry price to determine the actual position size in tokens.

4-2. Exception for the First Position (100% / 300%)

For the very first position (when there is no open position),

the strategy does not use the zone % parameters. Instead, it uses fixed ratios:

Default: Enter the first position with 100% of equity.

If the drawdown from ATH at that moment is greater than or equal to a predefined threshold (e.g. –72.5% or more)

→ Enter the first position with 300% of equity.

The position value is computed as:

Position Value = Current Equity × (100% or 300%) × Leverage

Then it is divided by the entry price to obtain the token quantity.

This rule:

Applies regardless of whether the first entry occurs at the 1st zone or 2nd zone.

Embeds the philosophy:

“In very deep crashes, go much larger on the first entry; otherwise, stay more conservative.”

4-3. Tracking Real Leverage

On each bar, the strategy tracks:

The existing position size at the start of the bar

The newly added size (if any) on that bar

When a new entry occurs, it calculates the real leverage at that moment:

Real Leverage = (Position Value / Current Equity)

This is then displayed on the chart as a label, for example:

Lev 2.53x

This makes it easy to see the actual leverage level at each entry point.

5. Visualization & Monitoring

5-1. On-Chart Visual Elements

The strategy plots the following directly on the chart:

ATH Line

The all-time high (based on High) is plotted as an orange line.

Average Entry Price Line

When a position is open, the average entry price of that position is plotted as a yellow line.

Estimated Liquidation Price (Fixed) Line

The strategy detects when the position size changes.

At each size change, it uses the current average entry price and real leverage to compute an approximate liquidation price.

This “fixed liquidation price” is then plotted as a red line on the chart.

If there is no position, or if leverage is 1x or lower, the liquidation line is removed.

Entry Markers & Labels

When 1st/2nd entry conditions are met, the strategy:

Marks the entry point on the chart.

Displays labels such as "Buy XX% @ Price" and "Lev XXx",

showing both entry percentage and real leverage at that time.

The label placement is configurable:

Below Bar

Above Bar

At Price

5-2. Information Table (Top-Right Panel)

In the top-right corner of the chart, the strategy displays a summary table of the current account and position status. It typically includes:

Pos Qty (Token)

Absolute size of the current position (in tokens)

Pos Value (USDT)

Market value of the current position (qty × current price)

Leverage (Now)

Current real leverage (position value / current equity)

DD from ATH (%)

Current drawdown (%) from the latest ATH, based on current price

Avg Entry

Average entry price of the current position

PnL (%)

Unrealized profit/loss (%) of the current position

Max DD (Equity %)

The maximum equity drawdown (MDD) recorded over the entire backtest period

Last Entry Price

Average entry price immediately after the most recent add-on entry

Last Entry Lev

Real leverage at the time of the most recent entry

Liq Price (Fixed)

The fixed estimated liquidation price described above

Return from Start (%)

Total return (%) of equity compared to the initial capital

Through this table, users can quickly grasp:

Current account and position status

Current risk level

Cumulative performance

6. Time Filters & Label Options

6-1. Strategy Date Range Filter

The strategy provides an option to restrict trading to a specific time range.

When “Use Date Range” is enabled:

You can specify start and end timestamps.

The strategy will only execute trades within that range.

When this option is disabled:

The strategy operates over the entire chart history.

6-2. Entry Label Placement

Users can customize where entry/leverage labels are drawn:

Below Bar (Below Bar)

Above Bar (Above Bar)

At the actual price level (At Price)

This allows you to adjust visualization according to personal preference and chart readability.

7. Use Cases & Applications

This strategy is suitable for the following purposes:

Long-term / swing-style re-buy strategies for spot or futures long positions

Testing rule-based strategies that rely on “drawdown from ATH” as a main signal

Monitoring account leverage, liquidation price, and MDD when using leverage

Handling situations where, for a given asset:

“Every time a new ATH is formed,

you want to wait for deep corrections and enter only at specific drawdown zones”

It is generally recommended to use this strategy not as a direct plug-and-play live system, but as a tool for:

Strategy idea validation

Risk profile analysis

Parameter exploration to match your personal risk tolerance and style

8. Limitations & Warnings

Backtest results do not guarantee future performance.

They are based on historical data only.

In live markets, additional factors exist:

Liquidity

Slippage

Fee structures

Exchange-specific liquidation rules

Funding fees, etc.

The liquidation price is only an approximate estimate, derived from a simplified formula.

Actual liquidation rules, maintenance margin requirements, fees, and other details differ by exchange.

The liquidation line should be treated as a reference indicator, not an exact guarantee.

Depending on the configured leverage and entry percentages, losses can be very large.

In particular, extremely aggressive settings such as “first position 300% of equity” can greatly increase the risk of large account drawdowns and liquidation during sharp market crashes.

Use such settings with extreme caution.

For live trading, additional risk management is essential:

Your own stop-loss rules

Maximum position size limits

Portfolio-level exposure controls

And other external safety mechanisms beyond this strategy

9. Conclusion

The ATH Drawdown Re-Buy Long Only strategy goes beyond simple “buy the dip” logic. It:

Systematically utilizes drawdowns from ATH as a structural signal

Applies a special first-position rule (100% / 300%)

Integrates visualization of leverage, liquidation price, MDD, and returns

All of this supports rule-based long position building in drawdown phases and comprehensive risk monitoring.

With this strategy, users can:

Explore different:

Drawdown zones

Entry percentages

Leverage levels

Run various backtests and scenario analyses

Better understand the risk/return profile that fits their own market view and risk tolerance

Once again, this strategy is intended for research, learning, and backtesting only.

All real trading decisions and their consequences are solely the responsibility of the user.

[Bybit BTCUSD.P] 7Years Backtest Results. 2,609% +Non-Repainting📊 I. Strategy Overview: Trust Backed by Numbers

The ADX Sniper v12 strategy has been rigorously tested over 7 years, from November 14, 2018 to November 8, 2025, spanning every major cycle of the Bitcoin

BTCUSD.P futures market. This strategy successfully balances two often-conflicting goals: maximizing profitability while minimizing volatility, all supported by objective performance data.

This strategy has been validated across all Bitcoin (BTCUSD.P) futures market cycles over a 7-year period.

■ Visual Proof: Bar Replay Simulation

The chart above demonstrates actual entry and exit points captured via TradingView's Bar Replay feature. The green rectangle highlights the core profitable trading zone, showing where the strategy successfully captured sustained uptrends. This visual evidence confirms:

Confirmed buy/sell signals with exact execution prices (marked in red and blue)

No repainting or signal distortion after candle close

Consistent performance across multiple market cycles within the highlighted zone

💰 Core Performance Metrics:

Cumulative Return: 2,609.14% (compounded growth over 7 years)

Maximum Drawdown (MDD): 6.999% (preserving over 93% of capital)

Average Profit/Loss Ratio: 8.003 (industry-leading risk-reward efficiency)

Total Trades: 24 (focused exclusively on high-conviction opportunities)

Sortino Ratio: 11.486 (mathematically proving robustness and stability)

✅ This strategy has been validated across all Bitcoin BTCUSD.P futures market cycles over a 7-year period.

📊 I. 전략 개요: 숫자로 입증된 신뢰

ADX Sniper v12 전략은 2018년 11월 14일부터 2025년 11월 8일까지 약 7년간 비트코인 (BTCUSD.P) 선물 시장의 모든 주요 사이클을 거치며 엄격하게 검증되었습니다. 수익성 극대화와 변동성 최소화라는 상충되는 목표를 동시에 달성한 이 전략의 핵심 성과 지표를 객관적 데이터를 통해 확인하실 수 있습니다.

본 전략은 7년간의 모든 비트코인 (BTCUSD.P) 선물 시장 사이클에서 검증되었습니다.

■ 시각적 증명: 바 리플레이 시뮬레이션

위 차트는 TradingView의 바 리플레이 기능으로 포착된 실제 진입 및 청산 시점을 보여줍니다. 녹색 네모는 핵심 수익 구간을 표시하며, 전략이 지속적인 상승 추세를 성공적으로 포착한 영역을 나타냅니다. 본 시각 자료는 다음을 입증합니다:

정확한 체결 가격이 표기된 확정된 매수/매도 신호 (빨강색과 파랑색으로 표시)

캔들 종가 후 신호 왜곡이나 리페인팅 없음

강조 표시된 구간 내 여러 시장 사이클에 걸친 일관된 성과

💰 핵심 성과 지표:

누적 수익률: 2,609.14% (7년간 복리 성장 입증)

최대 낙폭 (MDD): 6.999% (7년간 자본의 93% 이상 보존)

평균 손익비: 8.003 (업계 최고 수준의 위험-보상 효율성)

총 거래 횟수: 24회 (고확신 기회에만 집중)

소르티노 비율: 11.486 (전략의 견고성과 안정성을 수학적으로 입증)

✅ 본 전략은 7년간의 모든 비트코인 (BTCUSD.P) 선물 시장 사이클에서 검증되었습니다.

🛡️ II. Core Philosophy: Cut Losses Short, Let Profits Run

Why MDD Stays Below 7% in a Volatile Market

The crypto futures market typically experiences daily volatility exceeding 10%, with most strategies enduring drawdowns between 30% and 50%. In stark contrast, this strategy has never exceeded a 7% account loss over seven years. This exceptional low MDD is achieved through deliberate design mechanisms, not luck:

🎯 Entry Filtering: The 'ADX Pop-up Filter' is the core component. It enables the strategy to strictly avoid trading when market conditions indicate major reversals or consolidation phases, thereby minimizing exposure to high-risk zones.

🏛️ Capital Preservation Priority: The strategy prioritizes investor psychological stability and capital preservation over pursuing maximum potential returns.

The Power of an 8.003 Profit Factor

The Profit Factor measures the ratio of total profitable trades to total losing trades. It's the most critical metric for assessing risk-adjusted returns.

A Profit Factor of 8.003 means that for every dollar lost, the strategy earns an average of eight dollars. This demonstrates the efficiency of a true trend-following strategy:

Cutting losses quickly (averaging $177,419 USD loss per trade)

Riding winners for maximum extension (averaging $1,419,920 USD profit per trade)

🛡️ II. 핵심 철학: 손실은 빠르게 자르고, 수익은 끝까지

암호화폐 시장에서 MDD <7%의 의미

암호화폐 선물 시장은 일일 변동성이 10%를 초과하는 경우가 빈번하며, 일반적인 전략들은 30~50%의 MDD를 겪습니다. 이와 극명한 대조로, 본 전략은 7년간 단 한 번도 7%를 초과하는 계좌 손실을 기록하지 않았습니다. 이렇게 극도로 낮은 MDD는 운이 아닌 체계적인 메커니즘을 통해 달성되었습니다:

🎯 진입 필터링: 'ADX 팝업 필터'가 핵심 구성 요소로, 시장 상황이 주요 반전이나 횡보를 나타낼 때 거래를 엄격히 회피하여 고위험 구간 노출을 최소화합니다.

🏛️ 자본 보존 우선: 본 전략은 최대 잠재 손실을 감수하기보다 투자자의 심리적 안정성과 자본 보존을 우선시하도록 설계되었습니다.

손익비 8.003의 힘

손익비는 '총 수익 거래'와 '총 손실 거래'의 비율로, 위험 조정 수익을 측정하는 핵심 지표입니다.

8.003이라는 값은 1달러를 잃을 때마다 평균적으로 8달러 이상을 벌어들이는 구조를 의미합니다. 이는 진정한 추세 추종 전략의 최대 효율성을 보여줍니다:

손실은 빠르게 자르고 ($177,419 USD 평균 손실)

수익은 최대한 연장합니다 ($1,419,920 USD 평균 수익)

🎯 III. Strategy Reliability and Structural Edge

The Secret of 24 Trades in 7 Years

Only 24 trades over 7 years signifies that this strategy ignores 99% of market volatility and targets only the 1% of 'most certain buying cycles'. This approach eliminates the drag from excessive trading:

❌ No commission bleed

❌ No slippage erosion

❌ No psychological wear from overtrading

📈 Long-Term Trend Following: The strategy analyzes Bitcoin's long-term price cycles to capture the onset of massive trends while remaining undisturbed by short-term market noise.

Non-Repainting Structure: Alignment of Reality and Simulation

🎬 Non-Repainting Proof Video Available

※↑ "If you wish, I can also show you a video as evidence of the non-repainting throughout the 7 years."

✅ Real-Time Trading Reliability: This strategy is built with a non-repainting structure, generating buy/sell signals only after each candle's closing price is confirmed.

✅ Preventing Data Exaggeration: This design ensures that backtest results do not 'repaint' or distort past performance, guaranteeing high correlation between simulated results and actual live trading environments.

✅ Live Trading Advantage: While simulations use closing prices, live trading may allow entry at more favorable prices before candle close, potentially yielding even better execution than backtest results.

🎯 III. 전략의 신뢰성과 구조적 우위

7년간 24회 거래의 비밀

7년간 단 24회의 거래는 시장 변동성의 99%를 무시하고 오직 1%의 '가장 확실한 매수 사이클'만을 타겟으로 한다는 것을 의미합니다. 이는 과도한 거래로 인한 문제를 근본적으로 제거합니다:

❌ 수수료 소모 없음

❌ 슬리피지 침식 없음

❌ 과도한 트레이딩으로 인한 심리적 소모 없음

📈 장기 추세 추종: 비트코인 가격 역사를 지배하는 장기 사이클 분석을 활용하여, 단기 시장 노이즈에 흔들리지 않고 대규모 추세의 시작점을 포착하는 데 집중합니다.

논-리페인팅 구조: 현실과 시뮬레이션의 일치

🎬 논-리페인팅 증명 영상 제공 가능

※↑ "원하신다면 7년간 리페인팅이 없음을 증명하는 영상도 보여드릴 수 있습니다."

✅ 실시간 거래 신뢰성: 본 전략은 논-리페인팅 구조로 구축되어, 캔들의 종가가 확정된 후에만 매수/매도 신호를 생성합니다.

✅ 데이터 과장 방지: 이러한 설계는 백테스트 결과가 과거 성과를 '리페인팅'하거나 과장하지 않도록 보장하며, 시뮬레이션 결과와 실제 라이브 거래 환경 간의 높은 상관관계를 보장합니다.

✅ 라이브 실행 우위 가능성: 시뮬레이션은 종가 기준이지만, 라이브 운영 시 캔들이 마감되기 전 더 유리한 가격에 진입할 수 있어 시뮬레이션 결과보다 더 나은 실행 성과를 얻을 가능성이 있습니다.

📈 IV. Performance Summary (November 14, 2018 - November 8, 2025)

| Metric | Value || Metric | Value |

|--------|-------|

| Initial Capital | $1,000,000 |

| Net Profit | +$26,091,383.74 |

| Cumulative Return | +2,609.14% |

| Maximum Drawdown | -6.999% |

| Total Trades | 24 |

| Winning Trades | 19 (79.17%) |

| Losing Trades | 5 (20.83%) |

| Avg Winning Trade | +$1,419,920.16 |

| Avg Losing Trade | -$177,419.86 |

| Profit Factor | 8.003 |

| Sortino Ratio | 11.486 |

| Win/Loss Ratio | 8.003 |

⚙️ Default Settings:

Slippage: 0 ticks

Commission: 0.333% (Bybit standard)

📈 IV. 성과 지표 요약 (2018년 11월 14일 ~ 2025년 11월 8일)

|| 지표 | 값 |

|--------|-------|

| 초기 자본 | $1,000,000 |

| 순이익 | +$26,091,383.74 |

| 누적 수익률 | +2,609.14% |

| 최대 낙폭 | -6.999% |

| 총 거래 횟수 | 24 |

| 수익 거래 | 19 (79.17%) |

| 손실 거래 | 5 (20.83%) |

| 평균 수익 거래 | +$1,419,920.16 |

| 평균 손실 거래 | -$177,419.86 |

| 손익비 | 8.003 |

| 소르티노 비율 | 11.486 |

| 평균 손익 비율 | 8.003 |

⚙️ 기본 설정:

슬리피지: 0틱 (기본값)

수수료: 0.333% (Bybit 표준)

👥 V. Who Is This Strategy For?

✅ Long-term Bitcoin investors seeking stable, low-drawdown returns

✅ Traders tired of overtrading who prefer surgical, sniper-style precision entries

✅ Investors seeking psychological stability by avoiding large account swings

✅ Data-driven decision makers who value proven performance over marketing claims

👥 V. 이 전략은 누구를 위한 것인가요?

✅ 안정적이고 낮은 낙폭의 수익을 추구하는 장기 비트코인 투자자

✅ 과도한 매매에 지친 트레이더로 저격수 스타일의 정밀한 진입을 선호하는 분

✅ 큰 계좌 변동을 피하여 심리적 안정성을 추구하는 투자자

✅ 주장보다 검증된 객관적 성과를 중시하는 데이터 기반 의사 결정자

🔒 VI. Access & Disclaimer

🔐 Access Type: Invite-Only (Protected Source Code)

💬 How to Get Access: Send a private message or leave a comment below

⚠️ Important Disclaimer:

Past performance does not guarantee future results. Cryptocurrency and futures trading involve substantial risk of loss. This strategy is provided for educational and informational purposes only. Users should conduct their own research and consult with a financial advisor before making investment decisions. The author is not responsible for any financial losses incurred from using this strategy.

🔒 VI. 접근 방법 및 면책사항

🔐 접근 유형: 초대 전용 (소스코드 보호)

💬 접근 방법: 비공개 메시지 또는 아래 댓글 남기기

⚠️ 중요 면책사항:

과거 성과가 미래 결과를 보장하지 않습니다. 암호화폐 및 선물 거래는 상당한 손실 위험을 수반합니다. 본 전략은 교육 및 정보 제공 목적으로만 제공됩니다. 사용자는 투자 결정을 내리기 전 자체 조사를 수행하고 재무 자문가와 상담해야 합니다. 저자는 본 전략 사용으로 인한 재정적 손실에 대해 책임지지 않습니다.

🏷️ VII. Tags

Bitcoin |Bitcoin | BTCUSD | BTCUSD.P | Bybit | DailyChart | LongTerm | TrendFollowing | ADX | NonRepainting | Strategy | BacktestProven | SevenYears | LowDrawdown | HighProfitFactor | StableReturns | CapitalPreservation | Ichimoku | DMI | SuperTrend | TechnicalAnalysis | Volatility | RiskManagement | AutoTrading | Futures | PerpetualFutures | AlgorithmicTrading | SystematicTrading | DataDriven | InviteOnly | ProtectedScript | SnipperTrading | HighConviction | MDD | SortinoRatio

🏷️ VII. 태그

비트코인 |비트코인 | BTCUSD | BTCUSD.P | 바이비트 | 일봉 | 장기투자 | 추세추종 | ADX | 논리페인팅 | 전략 | 백테스트검증 | 7년검증 | 저낙폭 | 고손익비 | 안정수익 | 자본보존 | 일목균형표 | DMI | 슈퍼트렌드 | 기술적분석 | 변동성 | 위험관리 | 자동매매 | 선물 | 무기한선물 | 알고리즘트레이딩 | 시스템트레이딩 | 데이터기반 | 초대전용 | 보호스크립트 | 저격수트레이딩 | 고확신 | MDD | 소르티노비율

📌 Note: This strategy is designed exclusively for Bybit BTCUSD.P perpetual futures on the 1-day (daily) timeframe. Performance may vary significantly on other symbols or timeframes.

📌 참고: 본 전략은 Bybit BTCUSD.P 무기한 선물 계약의 1일봉(Daily) 타임프레임에 전용으로 설계되었습니다. 다른 심볼이나 타임프레임에서는 성과가 크게 달라질 수 있습니다.

[Bybit BTCUSD.P] 7Years Backtest Results. 2,609% +Non-Repainting

📊 I. Strategy Overview: Trust Backed by Numbers

The ADX Sniper v12 strategy has been rigorously tested over 7 years, from November 14, 2018 to November 8, 2025, spanning every major cycle of the Bitcoin BTCUSD.P futures market. This strategy successfully balances two often-conflicting goals: maximizing profitability while minimizing volatility, all supported by objective performance data.

This strategy has been validated across all Bitcoin (BTCUSD.P) futures market cycles over a 7-year period.

■ Visual Proof: Bar Replay Simulation

The chart above demonstrates actual entry and exit points captured via TradingView's Bar Replay feature. The green rectangle highlights the core profitable trading zone, showing where the strategy successfully captured sustained uptrends. This visual evidence confirms:

1) Confirmed buy/sell signals with exact execution prices (marked in red and blue)

2) No repainting or signal distortion after candle close

3) Consistent performance across multiple market cycles within the highlighted zone

💰 Core Performance Metrics:

Cumulative Return : 2,609.14% (compounded growth over 7 years)

Maximum Drawdown (MDD) : 6.999% (preserving over 93% of capital)

Average Profit/Loss Ratio : 8.003 (industry-leading risk-reward efficiency)

Total Trades : 24 (focused exclusively on high-conviction opportunities)

Sortino Ratio : 11.486 (mathematically proving robustness and stability)

✅ This strategy has been validated across all Bitcoin BTCUSD.P futures market cycles over a 7-year period.

🛡️ II. Core Philosophy: Cut Losses Short, Let Profits Run

Why MDD Stays Below 7% in a Volatile Market

The crypto futures market typically experiences daily volatility exceeding 10%, with most strategies enduring drawdowns between 30% and 50%. In stark contrast, this strategy has never exceeded a 7% account loss over seven years. This exceptional low MDD is achieved through deliberate design mechanisms, not luck:

🎯 Entry Filtering: The 'ADX Pop-up Filter' is the core component. It enables the strategy to strictly avoid trading when market conditions indicate major reversals or consolidation phases, thereby minimizing exposure to high-risk zones.

🏛️ Capital Preservation Priority: The strategy prioritizes investor psychological stability and capital preservation over pursuing maximum potential returns.

The Power of an 8.003 Profit Factor

The Profit Factor measures the ratio of total profitable trades to total losing trades. It's the most critical metric for assessing risk-adjusted returns.

A Profit Factor of 8.003 means that for every dollar lost, the strategy earns an average of eight dollars. This demonstrates the efficiency of a true trend-following strategy:

Cutting losses quickly (averaging $177,419 USD loss per trade)

Riding winners for maximum extension (averaging $1,419,920 USD profit per trade)

🎯 III. Strategy Reliability and Structural Edge

The Secret of 24 Trades in 7 Years

Only 24 trades over 7 years signifies that this strategy ignores 99% of market volatility and targets only the 1% of 'most certain buying cycles'. This approach eliminates the drag from excessive trading:

❌ No commission bleed

❌ No slippage erosion

❌ No psychological wear from overtrading

📈 Long-Term Trend Following: The strategy analyzes Bitcoin's long-term price cycles to capture the onset of massive trends while remaining undisturbed by short-term market noise.

Non-Repainting Structure: Alignment of Reality and Simulation

🎬 Non-Repainting Proof Video Available

※↑ "If you wish, I can also show you a video as evidence of the non-repainting throughout the 7 years."

✅ Real-Time Trading Reliability: This strategy is built with a non-repainting structure, generating buy/sell signals only after each candle's closing price is confirmed.

✅ Preventing Data Exaggeration: This design ensures that backtest results do not 'repaint' or distort past performance, guaranteeing high correlation between simulated results and actual live trading environments.

✅ Live Trading Advantage: While simulations use closing prices, live trading may allow entry at more favorable prices before candle close, potentially yielding even better execution than backtest results.

📈 IV. Performance Summary (November 14, 2018 - November 8, 2025)

|| Metric | Value |

|--------|-------|

| Initial Capital | $1,000,000 |

| Net Profit | +$26,091,383.74 |

| Cumulative Return | +2,609.14% |

| Maximum Drawdown | -6.999% |

| Total Trades | 24 |

| Winning Trades | 19 (79.17%) |

| Losing Trades | 5 (20.83%) |

| Avg Winning Trade | +$1,419,920.16 |

| Avg Losing Trade | -$177,419.86 |

| Profit Factor | 8.003 |

| Sortino Ratio | 11.486 |

| Win/Loss Ratio | 8.003 |

⚙️ Default Settings:

Slippage: 0 ticks

Commission: 0.333% (Bybit standard)

👥 V. Who Is This Strategy For?

✅ Long-term Bitcoin investors seeking stable, low-drawdown returns

✅ Traders tired of overtrading who prefer surgical, sniper-style precision entries

✅ Investors seeking psychological stability by avoiding large account swings

✅ Data-driven decision makers who value proven performance over marketing claims

🔒 VI. Access & Disclaimer

🔐 Access Type: Invite-Only (Protected Source Code)

💬 How to Get Access: Send a private message or leave a comment below

⚠️ Important Disclaimer:

Past performance does not guarantee future results. Cryptocurrency and futures trading involve substantial risk of loss. This strategy is provided for educational and informational purposes only. Users should conduct their own research and consult with a financial advisor before making investment decisions. The author is not responsible for any financial losses incurred from using this strategy.

🏷️ VII. Tags

Bitcoin |Bitcoin | BTCUSD | BTCUSD.P | Bybit | DailyChart | LongTerm | TrendFollowing | ADX | NonRepainting | Strategy | BacktestProven | SevenYears | LowDrawdown | HighProfitFactor | StableReturns | CapitalPreservation | Ichimoku | DMI | SuperTrend | TechnicalAnalysis | Volatility | RiskManagement | AutoTrading | Futures | PerpetualFutures | AlgorithmicTrading | SystematicTrading | DataDriven | InviteOnly | ProtectedScript | SnipperTrading | HighConviction | MDD | SortinoRatio

📌 Note: This strategy is designed exclusively for Bybit BTCUSD.P perpetual futures on the 1-day (daily) timeframe. Performance may vary significantly on other symbols or timeframes.

W%R Pullback+EMA Trend [TS_Indie]🔰 Core Concept of the Strategy

The main idea is “Trend-Following with Momentum Pullback.”

This means trading in the direction of the main trend (defined by EMA) while using Williams %R to identify pullback entries (buying the dip or selling the rally) where momentum returns to the trend direction.

📊 Indicators Used

1. EMA Fast – Defines the short-term trend.

2. EMA Slow – Defines the long-term trend (used as a trend filter).

3. Williams %R

• Overbought zone: above -20

• Oversold zone: below -80

⚙️ Entry Rules

🔹 Buy Setup

1. EMA Fast > EMA Slow → Uptrend condition.

2. Williams %R on the previous candle dropped below -80, and on the current candle, it crosses back above -80 → indicates momentum returning to the upside.

3. Current close is above EMA Fast.

4. Entry Buy at the close of the candle where %R crosses above -80.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the lowest low between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

🔹 Sell Setup

1. EMA Fast < EMA Slow → Downtrend condition.

2. Williams %R on the previous candle went above -20, and on the current candle, it crosses back below -20 → indicates renewed selling momentum.

3. Current price is below EMA Fast.

4. Entry Sell at the close of the candle where %R crosses below -20.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the highest high between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

⚙️ Optional Parameters

• Custom Risk/Reward Ratio for Take Profit.

• Option to add ATR buffer to Stop Loss.

• Adjustable EMA Fast period.

• Adjustable EMA Slow period.

• Adjustable Williams %R period.

• Option to enable Long only / Short only positions.

• Customizable Backtest start and end date.

• Customizable trading session time.

⏰ Alert Function

Alerts display:

• Entry price

• Stop Loss price

• Take Profit price

Guys, try adjusting the parameters yourselves!

I’ve been tweaking the settings for several days and managed to get great results on XAU/USD in the 5-minute timeframe.

I think this strategy is quite interesting and could potentially deliver good results on other instruments as well.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only.

It does not guarantee profits and should not be considered financial advice.

Trading in financial markets involves significant risk, including the potential loss of capital.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.